With Republican legislative leaders and Democratic Gov. Tony Evers having reached and passed a budget deal for Wisconsin’s 2025-27 biennium (fiscal years 2026 and 2027), it is worth examining two significant tax relief proposals Republicans included in their plan.

The more costly of the two provisions, reducing individual income tax collections by an estimated $695 million over two years, is a significant increase in the amount of retirement income that is excluded from income taxes for Wisconsin seniors. The next most expensive provision, reducing collections by an estimated $643 million over the biennium, expands the amount of income that falls within Wisconsin’s second-lowest bracket.

If the goal of the bracket threshold change is to provide tax relief to lower- and middle-income Wisconsinites, expanding the amount of income that is exposed to the lower 4.4 percent rate, rather than the 5.3 percent rate, is a relatively well-structured way to accomplish that goal. However, the expanded retirement income exclusion will undermine the tax code’s neutrality and shift burdens onto working families over time, while yielding far less “bang for the buck” than other more pro-growth reforms.

Retirement income exclusion

Republicans’ proposal, passed by the Legislature and signed by Evers early Thursday morning, substantially expands Wisconsin’s retirement income exclusion by increasing the maximum exclusion amount from $5,000 to $24,000 for single filers and from $10,000 to $48,000 for married couples filing jointly. While eligibility is limited to those who are at least 67 years of age, up from 65 years of age, the exclusion is no longer income-tested.

While well-intentioned as a way to provide tax relief to retirees facing financial strain and to help Wisconsinites stay in Wisconsin, the measure goes far beyond that by wiping out income tax liability altogether for many retirees and by substantially reducing income tax liability for even the affluent.

Imagine a married couple with $60,000 in non-Social Security retirement income. Under current law, this couple would be ineligible to claim Wisconsin’s income-tested retirement income exclusion of $10,000 because their federal adjusted gross income (AGI) exceeds $30,000. If they claim Wisconsin’s standard deduction ($18,823 in tax year 2025 for a couple with $60,000 in Wisconsin income) and personal exemptions ($1,900 for a married couple with both individuals ages 65 or over), their Wisconsin taxable income would be $39,277, and their total income tax liability would be approximately $1,553 under Wisconsin’s current rate schedule.

Under the just-passed measure, if this couple takes at least $48,000 in distributions from qualifying retirement accounts, this would reduce their Wisconsin income to only $12,000. After claiming the standard deduction, they would have $0 in taxable income and would not be required to pay any income taxes to Wisconsin.

A separate retired couple with $100,000 in federal AGI would have only $52,000 in Wisconsin income once the $48,000 retirement income exclusion is claimed. Since Wisconsin’s sliding-scale standard deduction varies based on a taxpayer’s Wisconsin income after exclusions are applied, the retirement income exclusion would enable this couple to claim a higher standard deduction than they would have been able to claim otherwise. Specifically, they would be able to claim a $20,405 standard deduction and a $1,900 personal exemption, reducing their Wisconsin taxable income to $29,695. Under both Wisconsin’s old and just-passed rate schedules, this would yield a tax liability of approximately $1,130.

Meanwhile, a working-age couple with $100,000 in federal AGI would be eligible to claim a standard deduction of only $10,911, reducing their taxable income to $87,689 once their $1,400 personal exemption is applied. Under Wisconsin’s old income tax rates, this would yield an income tax liability of approximately $4,119. Under the budget’s new rate schedule with the expanded 4.4 percent bracket, this would yield a liability of approximately $3,866. As such, under either the old brackets or the new schedule, the working-age taxpayers making $100,000 would pay roughly three-and-a-half times more than the retired taxpayers despite having the same amount of annual income.

Such a large retirement income exclusion injects significant non-neutrality into Wisconsin’s tax code, extending preferential treatment to older Wisconsinites over working-age individuals and families. Such a sharp tax cut for retirees, including those with comfortable retirement savings and additional accrued wealth, will, over time, put upward pressure on the income tax rates that would apply to the narrower base of primarily working-age Wisconsinites. This could create an incentive for more seniors to move to Wisconsin from other states to take advantage of this preferential treatment, putting additional strain on state coffers, even as working-age Wisconsinites may become more likely to relocate to low- or no-income-tax states.

It is important to keep in mind, especially when thinking about income incurred in retirement, that annual income alone is not a sufficient proxy for wealth or ability to pay. Some retirees take relatively modest annual distributions from their retirement accounts while retaining other high-value assets, such as vacation properties or other non-retirement account investments. Furthermore, after saving and investing for decades, many older Americans are actually better able to afford state income tax payments than their working-age children, friends, and neighbors who haven’t yet accrued many assets and are still working to pay down student loans and mortgages.

Additionally, while reducing (and in some cases eliminating) income taxes on retirees gives them more capacity for additional consumption, which could have a positive effect on sales tax revenues, a large retirement income exclusion is far less likely to promote long-term economic growth in Wisconsin than income tax relief — especially income tax rate reductions — that reduce the burden on economic growth-inducing activities like labor and investment.

Instead of substantially expanding the retirement income exclusion, policymakers should instead have reduced income tax rates or otherwise made the income tax code friendlier for all taxpayers, including retirees as well as members of Wisconsin’s current workforce. To the extent Wisconsin policymakers wish to further relieve tax burdens for fixed-income individuals who are truly struggling to make ends meet, policymakers could consider making additional age- and/or income-tested provisions more generous. A more reasonable, targeted solution would be to modestly increase the income threshold for the existing $5,000 per person retirement income exclusion, and perhaps index it to inflation, to ensure more claimants actually benefit from it.

Expansion of second-lowest individual income tax bracket

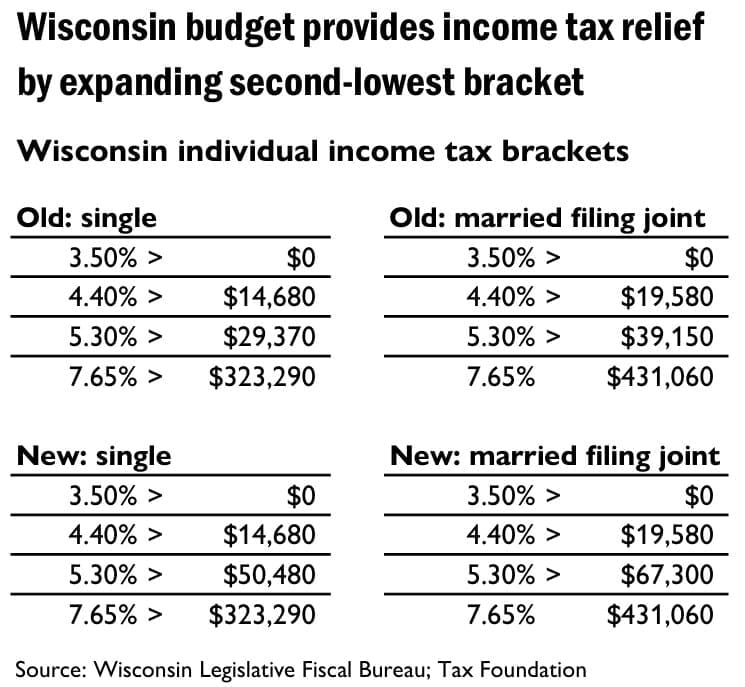

In addition to substantially expanding the retirement income exclusion, Republicans’ tax plan as passed provides individual income tax relief to lower- and middle-income taxpayers by expanding Wisconsin’s second-lowest individual income tax bracket, retroactively effective as of tax year 2025. Specifically, the measure applies the 4.4 percent rate, rather than the 5.3 percent rate, to an additional $21,110 in taxable income for single filers and an additional $28,150 in taxable income for married couples filing jointly, as shown in the table below.

This change is a structurally sound way to provide individual income tax relief to lower- and middle-income taxpayers. Until this budget, Wisconsin’s second-highest individual income tax rate of 5.3 percent kicked in at only $29,370 in taxable income for single filers and $39,150 for married couples filing jointly. As such, a large number of lower-income Wisconsinites were exposed to Wisconsin’s second-highest rate. Specifically, Wisconsin until now imposed a higher marginal income tax rate on $30,000 in taxable income for single filers than is imposed in all but 10 states (Delaware, Hawaii, Kansas, Maine, Minnesota, Montana, New York, Oregon, South Carolina, Virginia) and the District of Columbia.

Katherine Loughead is a senior policy analyst and research manager with the Center for State Tax Policy at the Tax Foundation and author of the Badger Institute’s Tax Reform Options to Improve Wisconsin’s Competitiveness.

This is an updated version of a brief published July 2 by the Tax Foundation. Published with permission of the Tax Foundation.

Submit a comment

Go to the full page to view and submit the form.