July 13, 2022— Over the past two years, a wave of tax reform has swept the country—particularly in the Midwest. While Wisconsin trimmed its lowest three income tax rates, it was not among the states to enact comprehensive reform, and the state’s competitiveness is suffering as a result.

Given Wisconsin’s strong budget surplus and continued projected revenue growth, policymakers have a solid opportunity to continue to rebalance Wisconsin’s tax structure by shifting reliance away from economically harmful taxes on productivity and toward less harmful taxes on consumption.

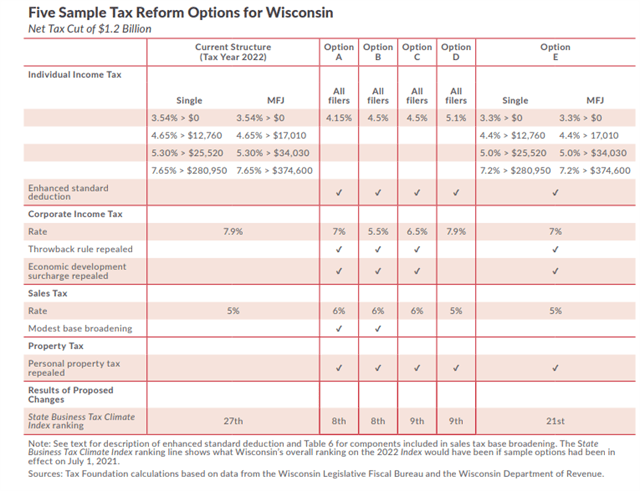

A new report from the Washington, D.C.-based Tax Foundation and the Milwaukee-based Badger Institute, titled Tax Reform Options to Improve Wisconsin’s Competitiveness, lays out five comprehensive tax reform options to enhance Wisconsin’s tax competitiveness with a focus on reducing economically harmful taxes on labor and investment.

Five Tax Reform Options:

If Wisconsin policymakers were to enact any of the proposed tax reform options, the state would substantially increase its ranking on the Tax Foundation’s State Business Tax Climate Index, positioning itself for long-term economic growth.

The five sample reform options show how these specific policy changes could be combined in various ways to offer a net tax cut of approximately $1.2 billion:

- Reduce the Top Marginal Individual Income Tax Rate: Since 2019, Wisconsin’s three lowest individual income tax rates have been reduced, but the top rate remains unchanged. At 7.65 percent, Wisconsin’s top rate is higher than the rates in all but eight states and the District of Columbia, reducing returns to labor and investment on the margin.

- Consolidate Four Individual Income Tax Brackets Into One: In 2022 alone, four states enacted legislation or received court clearance to move to a single-rate income tax structure. There are now 13 states that now already have or are moving toward a flat tax. Consolidating four brackets into one would better promote upward mobility and economic growth in Wisconsin.

- Reduce the Corporate Income Tax Rate: Regarded by economists as the most economically harmful of the major state revenue sources, the corporate income tax falls on workers, consumers, and shareholders, hindering economic opportunity and growth. Many states have reduced reliance on corporate taxes in recent years, but not once in its history has Wisconsin’s corporate income tax rate been reduced.

- Increase the Standard Deduction: Wisconsin’s sliding-scale standard deduction is income-tested, with the amount taxpayers are eligible to claim decreasing as income increases. To provide additional targeted tax relief to those at the lower end of the income spectrum, our five tax reform options increase both the maximum standard deduction and the amount of income at which the deduction phases down.

- Repeal the Economic Development Surcharge: In addition to corporate or individual income tax liability, many Wisconsin businesses must pay an economic development surcharge to fund the Wisconsin Economic Development Corporation (WEDC). Compared to the current surcharge that is levied only on select businesses, the general fund would be a more neutral and stable source of revenue for the WEDC. As such, we propose repealing the economic development surcharge and instead funding the WEDC through the general fund.

- Repeal the Throwback Rule: The throwback rule in Wisconsin’s corporate income tax code reduces Wisconsin’s tax competitiveness, adds unnecessary complexity, and creates the potential for double taxation. Repealing the throwback rule would enhance Wisconsin’s future growth prospects.

- Repeal the Tangible Personal Property Tax: While commendable progress has been made to reduce reliance on tangible personal property taxes over time, some property remains taxable, such as office furniture, fixtures, and equipment, as well as boats and other watercraft. Wisconsin policymakers have already set aside revenue to repeal this tax, but the tax will continue to be collected until lawmakers enact legislation removing it from the books.

- Partially Offset Income Tax Reforms With Sales Tax Base Broadening or Rate Increases: Wisconsin’s sales tax rate is among the lowest in the country, and the sales tax does not yet apply to certain consumer services and goods. If policymakers wish to offset a portion of income tax reforms, they could do so through modest sales tax base broadening or rate increases, but only three of our five options propose any offsets.

“Wisconsin’s individual and corporate income taxes are among the highest in the nation. In a post-pandemic economy where workers and businesses are more mobile than ever, the state needs to take those taxes head on if it wants to keep up with other states in the Midwest and nationwide,” said Katherine Loughead, senior policy analyst at the Tax Foundation. “Given the state’s strong budget surplus and projected continued revenue growth, Wisconsin is in a prime position to enact pro-growth reforms to improve the state’s competitive standing for decades to come.”

“Our neighbors, Illinois and Michigan, already have flat taxes and Iowa will soon as well,” said Badger Institute President Mike Nichols. “Indiana, another Midwestern state we compete with for businesses and jobs, has a flat tax too. Why are we so timid, so lackadaisical and uncompetitive? It’s time for us to join the modern world, acknowledge we’re getting left behind. We can’t prosper without tax reform.”