State government needn’t have a hand in retirement-savings fix; private-sector options already proliferate

Editor’s note: “The natural progress of things is for liberty to yield, and government to gain ground,” Thomas Jefferson famously wrote in 1788. “As yet,” he added, “our spirits are free.” Some 231 years later, they might not be much longer if government leaders and bureaucrats continue trying to take over traditional private-sector enterprises like housing development, retirement planning and lending. Our package of stories looks at how government is trying to insert itself into these arenas.

First it was the deep blue states — California, Illinois and Oregon — inserting government into the private-sector arena of retirement planning. In recent years, all have ordered employers that don’t offer retirement plans to automatically enroll workers into state-sponsored plans unless they explicitly opt out.

Now Wisconsin political leaders of both stripes are exploring whether to follow suit.

Gov. Tony Evers has established a Retirement Security Task Force, led by state Treasurer Sarah Godlewski, to study the retirement-savings problem in Wisconsin and make recommendations accordingly.

Not to be outdone, Republican state Reps. Jon Plumer of Lodi and Cindi Duchow of Delafield in late August unveiled a proposed pilot program called REvest that mimics the state-run, mandated retirement plans launched in other states. A bill has not yet been drafted.

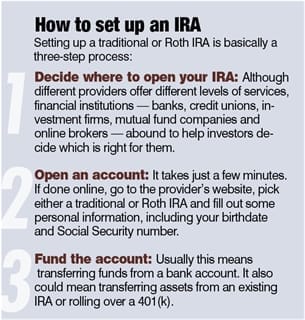

But is state involvement necessary? The question warrants scrutiny because state-sponsored individual retirement accounts, or auto-IRAs, don’t actually fill a void. Traditional and Roth IRAs already proliferate in the private sector. They can be set up at local financial institutions or online, and many don’t even require a minimum contribution. From start to finish, the whole process is relatively simple.

State governments jumping into the mix could prove harmful not only to private-sector IRA providers competing in the same arena but also — and more important — to the targeted employers and employees themselves.

Workers’ other priorities

There are many reasons employees don’t save for retirement. To be sure, some of it is due to ignorance, sheer inertia or negligence. In most instances, however, the workers have other costs or debts that demand more immediate attention. As they should.

For example, paying off high-interest credit card debt makes a lot more economic sense than setting aside money in a state-sponsored retirement fund growing at a much slower rate, the Cato Institute explains.

To illustrate the point, Cato notes: “At an 18% interest rate, an unpaid $5,500 credit card debt would mushroom to $28,800 in 10 years. The same amount of money directed toward OregonSaves (one of the state-sponsored plans in effect) might accumulate $12,900 under rosy assumptions about investment returns.”

A local retirement planning expert has witnessed the employees’ dilemma. “Nearly 20 years of experience dealing with American workers has taught me that most people understand they should save for retirement, and they genuinely want to do so. Credit card debt, student loans, living paycheck to paycheck and other budgetary challenges simply prevent them from saving,” says Tom Parks, director of Retirement Plan Services at Annex Wealth Management in Elm Grove.

As for those who can, do and will save, they don’t need government to add another retirement plan to the ones already available in the private sector.

Certainly, financial advisors in the private sector would agree. “Our members, they market retirement products. They don’t see any reason, quite frankly, to compete with the state,” Gary Sanders of the National Association of Insurance and Financial Advisors (NAIFA) told Employee Benefit Adviser.

The Oregon program and employers

It is worthwhile to examine the features of OregonSaves, the first plan of its kind and considered a prototype for other states to follow. Oregon launched the program in 2017.

For starters, even though employers without retirement plans don’t pay into the state-run plan, Oregon mandates that they automatically enroll their employees (save for those who opt out) and deduct 5% from employees’ paychecks as contributions to the plan. The deductions increase by 1% per year until 10% is reached. Other requirements also apply. If employers fail to comply, they get dinged with a penalty that can ratchet up to $5,000 per year.

Many of these small business owners might not welcome new mandates rammed down their collective throats. As Annex’s Parks told the Badger Institute, “From the perspective of employers, one of the most problematic aspects of a state-sponsored retirement plan is the administrative burden it would place on small businesses.”

Retirement financial advisors in Oregon share that concern. “Most business owners are naturally suspicious and frustrated by another government mandate,” Ashley Micciche, CEO of True North Retirement Advisors in Clackamas, told Employee Benefit Adviser. And Tim Wood of Foster & Wood Retirement Plan Advisors in Lake Oswego quotes a CFO of a business hit by the mandate as saying, “Why would we want the same people that run the DMV running our retirement plan?”

That sentiment is echoed in Wisconsin. The state-sponsored plans “should be inexpensive to operate, but they won’t be because they will never be more than small accounts and run by an inefficient bureaucracy,” says Robert Kieckhefer, a longtime retirement specialist who founded The Kieckhefer Group in Brookfield.

The effect on employees

Of course, the proof is in the pudding, and so far it would appear that the pudding doesn’t taste all that good.

Although the rollout of OregonSaves continues into 2020 with many employers yet to be reached, as of the end of 2018, 47,000 workers out of a potential total of 1 million had enrolled. Of those 47,000, only 23,000 workers actually had contributed.

For the employees, restrictions abound: 1) the percentage contribution is fixed; 2) their first $1,000 gets put (no choice) into a stabilization fund that since its inception has earned 1.52% per annum, or basically 0% after factoring in inflation; 3) if and when they have more than $1,000 invested, they must choose between a fund that is a mixture of stocks and bonds and one that is invested entirely with the State Street Equity 500 Index Fund; and 4) the only retirement vehicle available is a Roth IRA. In short, not quite a “one size fits all” retirement solution but close.

For comparison, in the private sector, Vanguard offers multiple low-cost, exchange-traded and mutual funds listed among Money magazine’s “best of” funds for 2019 — most of which averaged an annual return of over 10% during the most recent 10-year period. Further, Vanguard has its own well-established target retirement funds.

Vanguard, of course, is not alone. Fidelity, Principal and countless other firms distribute comparable, retirement-focused products. Directing employees away from these superior investment products arguably does a disservice to the workers themselves as well as to providers competing in the same marketplace.

Even more insidious is the prospect that some employers currently offering retirement benefits would drop their own plans — for example, 401(k)s that often have attractive employer-matching contributions — if they expected the state to pick up the slack.

All of this is not to say there isn’t an acute problem. More than 50% of working Wisconsinites have less than $3,000 saved for retirement, Godlewski says. However, the state should not mandate a faux solution when real solutions already exist in the private sector.

Jay Miller of Whitefish Bay is tax attorney and a visiting fellow at the Badger Institute.

Related stories:

► The limited role for government in easing retirement-savings problem

► No need for state-run student loan refinancing

► Government’s unfair housing foray

► Opportunity Zones stray from original intent

► A Housing Authority subsidiary with a social mission